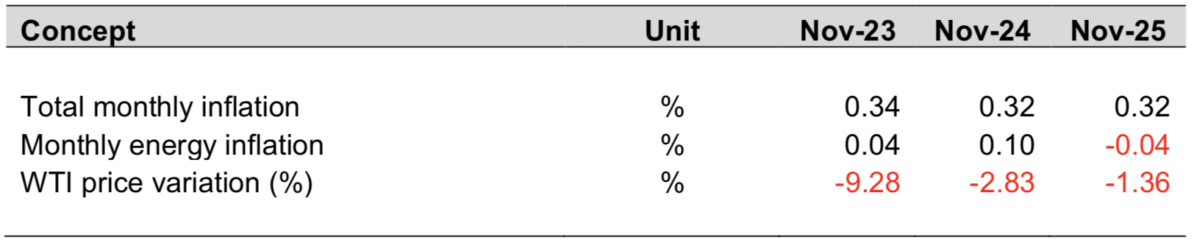

The Energy Inflation recorded a decrease in November 2025, dropping from 0.19% in October to –0.04% in November. This behavior is mainly explained as 11 of the 20 countries analyzed recorded a decline in the indicator, in a context where several countries implemented regulatory measures aimed at stabilizing electricity prices. Additionally, the region benefited from the decline in international oil prices, driven by higher global supply in the second half of 2025, which reduced fuel import costs for both the transport sector and thermal power generation.

On the other hand, although a rebound in the price of natural gas in North America was observed towards November, associated with increased demand and seasonal weather conditions, this factor exerted only partial upward pressure in LAC; the combined effects of the oil drop and tariff measures prevailed widely, generating a net regional downward impact mainly due to the weight of oil-derived fuel prices and electricity prices in the energy basket.

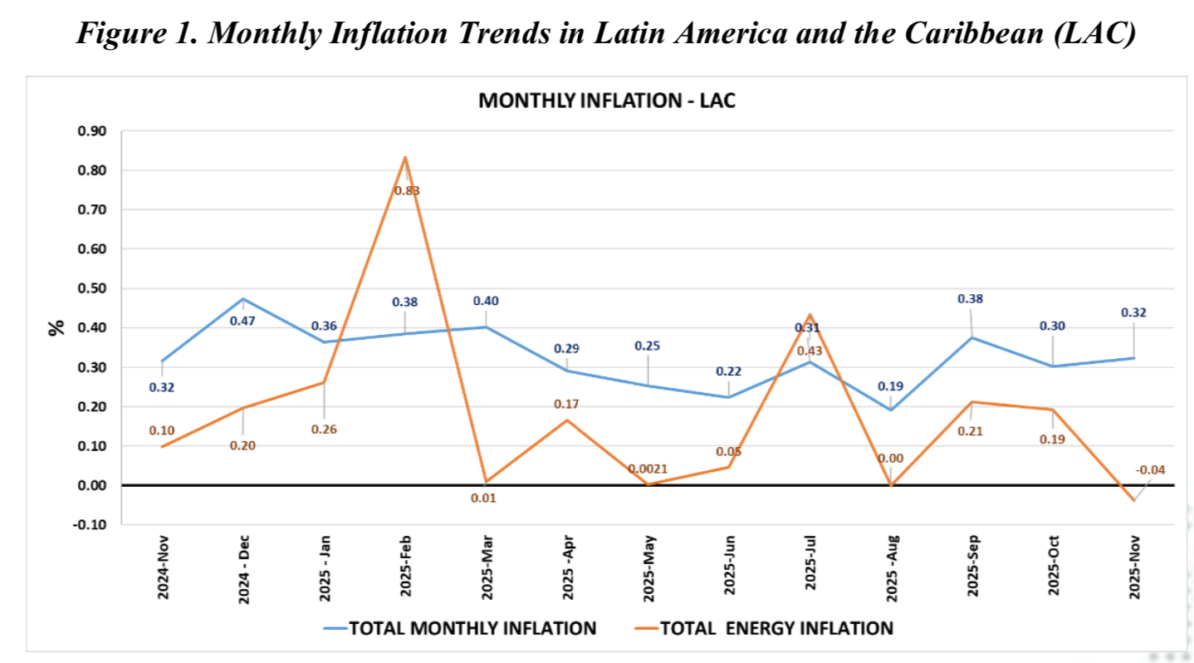

In contrast, total monthly inflation moved in the opposite direction to energy inflation, rising by 0.32% in November 2025, indicating that the increase was driven by components other than energy, such as food, goods, and services, which carry greater weight in the index.

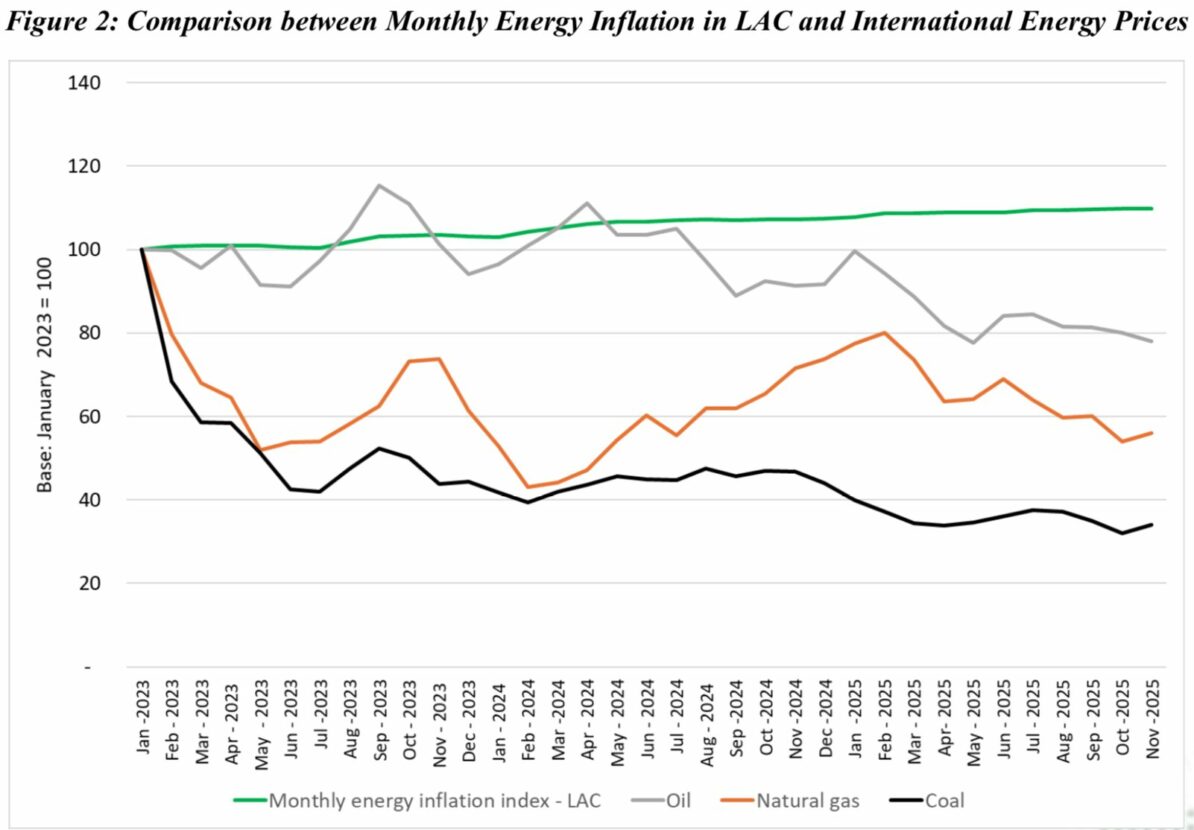

Figure 2 shows that the international oil price index throughout 2025 dominated a downward trend due to a greater supply and accumulation of global inventories, with decreases that contributed to alleviating energy inflation in LAC, especially in the second half of 2025.

On the other hand, the natural gas price index shows periods of recovery in mid-2024 and part of 2025 and a rebound in November 2025 due to a seasonal increase in demand and greater dynamism of LNG in the United States, which tends to pressure the increase in electricity rates of dependent gas systems. However, this impulse was not enough to reverse the fall in the energy inflation index in November 2025, which reached a negative value.

Regarding the coal price index, the performance is downward over the analysis period with some stabilization towards the second half of 2025. In the international context, prices showed year-on-year adjustments reaching negative values at the end of 2025, which also contained generation costs in matrices with thermal participation in mineral coal.

In general terms, Figure 2 shows that the energy inflation index in LAC is less volatile than oil, natural gas, and coal, although it tracks the downward trend in oil prices during the second half of 2025. The one-off rise in natural gas at the end of 2025 did not prevent energy inflation from closing with a negative value at the end of November 2025.